The saudi oncology market is moving fast toward more precise care, but access and delivery still decide what patients can actually receive. Across the Middle East, cancer drug demand is linked to rising cancer prevalence, advancements in drug development, and rising healthcare expenditure. Saudi Arabia is repeatedly listed among the countries that dominate regional oncology and supportive care markets due to advanced healthcare infrastructure, high investment in oncology research, and a growing number of cancer treatment centers.

Several sources point to the therapy shift that matters for 2026 planning. The Middle East oncology drugs market includes chemotherapy drugs, targeted therapy drugs, immunotherapy drugs, hormonal therapy drugs, biosimilars, and combination therapy drugs. Targeted therapy drugs are described as gaining traction because they specifically target cancer cells, which can support better outcomes and reduced side effects. In breast cancer treatment, Saudi Arabia is also seeing growing use of personalized and precision oncology, plus expanded immunotherapy and hormonal therapy options.

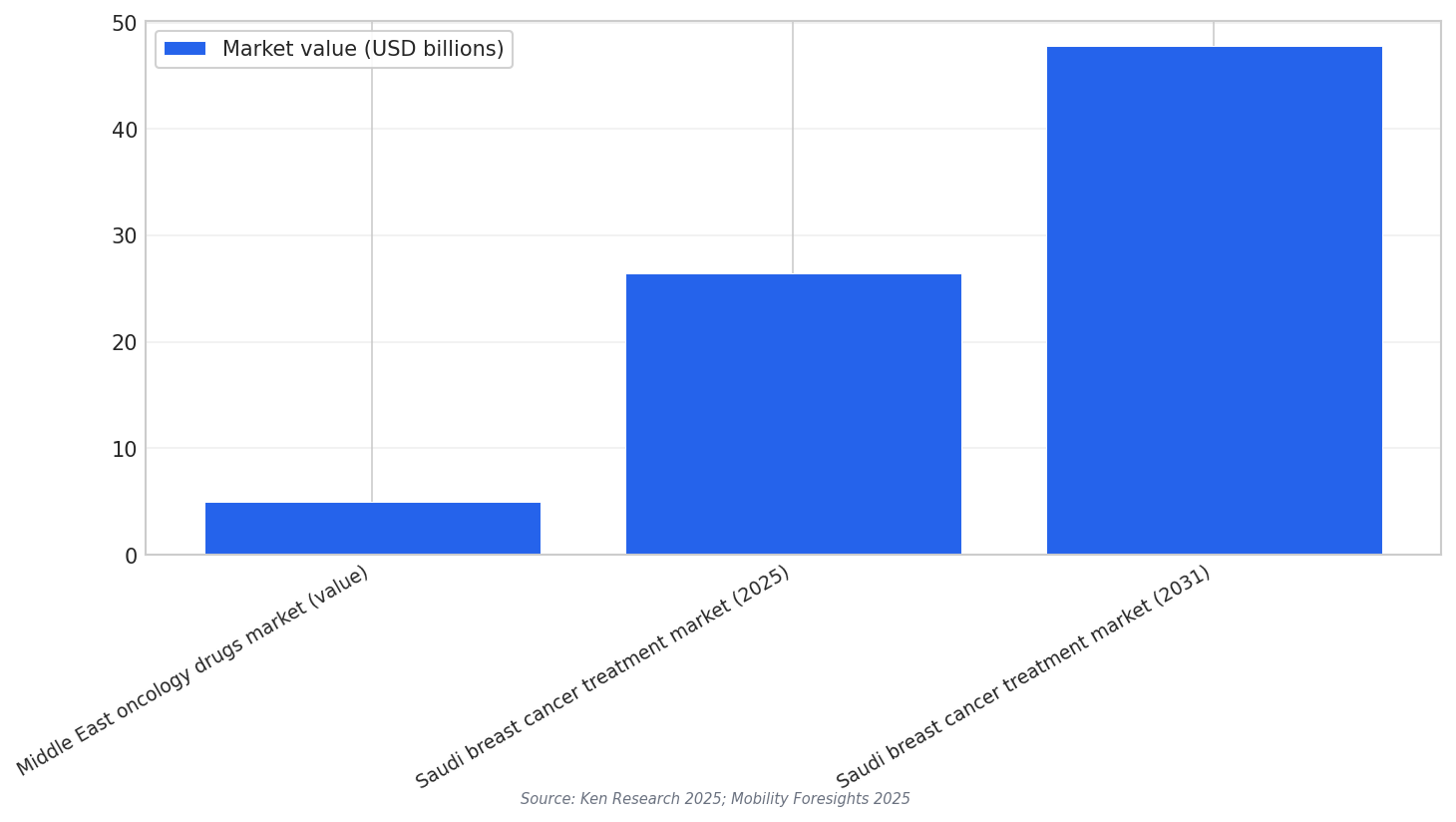

On the numbers side, three data points help show the scale and direction of oncology spending discussed in the sources. The Middle East oncology drugs market is valued at approximately USD 5 billion. In one Saudi-specific segment, the Saudi Arabia Breast Cancer Treatment Market is projected to grow from USD 26.4 billion in 2025 to USD 47.8 billion by 2031. These values are not the same market definition, but together they show how large single-cancer treatment segments can be, while regional drug markets are also expanding.

Cancer Centers and the Access Gap That Shapes Outcomes

Care access is not only about which drugs exist. It is also about where specialized services are located. In Saudi Arabia, access to specialized cancer care is described as a challenge, particularly in rural areas, because specialized oncology services are concentrated in major urban centers. One source states that approximately 62% of the population lives outside major urban centers, which helps explain why patients can face uneven access to oncology specialists and advanced diagnostics.

Drug access in 2026 will also be influenced by cost and treatment pathways. In breast cancer, increasing availability of biosimilars is described as reducing treatment costs and expanding patient access. Sources also emphasize the rise of molecular profiling technologies and biomarker profiling to guide precision oncology. This matters because treatment selection can depend on subtype, stage, age, and molecular characteristics, which raises the value of accurate testing and diagnostics.

Supportive care is another part of the care outlook. Saudi Arabia is listed among countries that dominate the Middle East cancer supportive care drugs market due to advanced infrastructure, high investment in oncology research, and more cancer treatment centers. The same supportive care source links growth to improving quality of life for patients undergoing cancer therapies and to expanding healthcare infrastructure with government initiatives under programs like Saudi Vision 2030. Together, these themes suggest a 2026 outlook focused on wider treatment choice, better-guided therapy, and steady work to close access gaps beyond the biggest cities.

What is changing most in the saudi oncology market for 2026?

Why do cancer centers and location matter for access in Saudi Arabia?

What market figures in the sources show oncology growth signals?

What role do supportive care drugs play in the care outlook?