Saudi Arabia’s clinical research landscape is being reshaped by regulatory reform and growing operational capacity. In the Middle East, supportive government policies and investments in healthcare infrastructure are highlighted as key growth drivers for clinical trial activity, alongside demand for innovative therapies and an emphasis on personalized medicine. One regional market view values the Middle East clinical trials market at USD 2.5 billion in 2024 and projects it to reach USD 5.0 billion by 2034, with a 7.5% CAGR. Within that regional momentum, Saudi Arabia is repeatedly cited as a country implementing reforms to streamline approval processes, creating clearer pathways for sponsors to start studies.

Regulatory streamlining is not only a policy theme; it is tied directly to execution. In Saudi Arabia, the Saudi Food and Drug Authority (SFDA) is described as implementing regulatory reforms that support faster trial approvals, facilitating CRO activities and encouraging more pharmaceutical companies to conduct trials in the country. This matters because demand is rising. Ken Research cites over 7 million people affected by diabetes alone in Saudi Arabia, underscoring the chronic disease burden that drives research interest. Across the broader Middle East, the World Health Organization (WHO) estimates non-communicable diseases account for approximately 70% of all deaths in the region, reinforcing why sponsors prioritize studies in diabetes, cardiovascular diseases, and cancer.

CRO Capacity and Trial-Tech Tools Are Scaling Up

As regulatory processes become more navigable, service capacity is also expanding. In Saudi Arabia’s pharmaceutical CRO landscape, clinical research services are described as the top segment, with clinical trial services spanning early-stage and post-marketing research. The market itself is valued at approximately USD 236 million, driven by demand for clinical trials, chronic disease prevalence, and government investments in healthcare infrastructure. The same ecosystem includes local providers offering functions such as regulatory support, clinical trial administration, biostatistics, and medical writing, helping sponsors operationalize trials under stricter compliance expectations and evolving review requirements.

Technology is another lever for speed and compliance. The Saudi Arabia Clinical Trial Management Systems (CTMS) market is valued at approximately USD 150 million, supported by the need for efficient management of clinical data and regulatory compliance. This demand is linked to volume growth: Ken Research notes that the number of clinical trials conducted in Saudi Arabia has increased significantly, with over 1,500 active trials reported in future. That same source attributes the surge to the growing pharmaceutical and biotechnology sectors, which are expected to invest around SAR 20 billion (USD 5.3 billion) in research and development by future. As trials expand, CTMS becomes central to document control, data handling, and audit readiness.

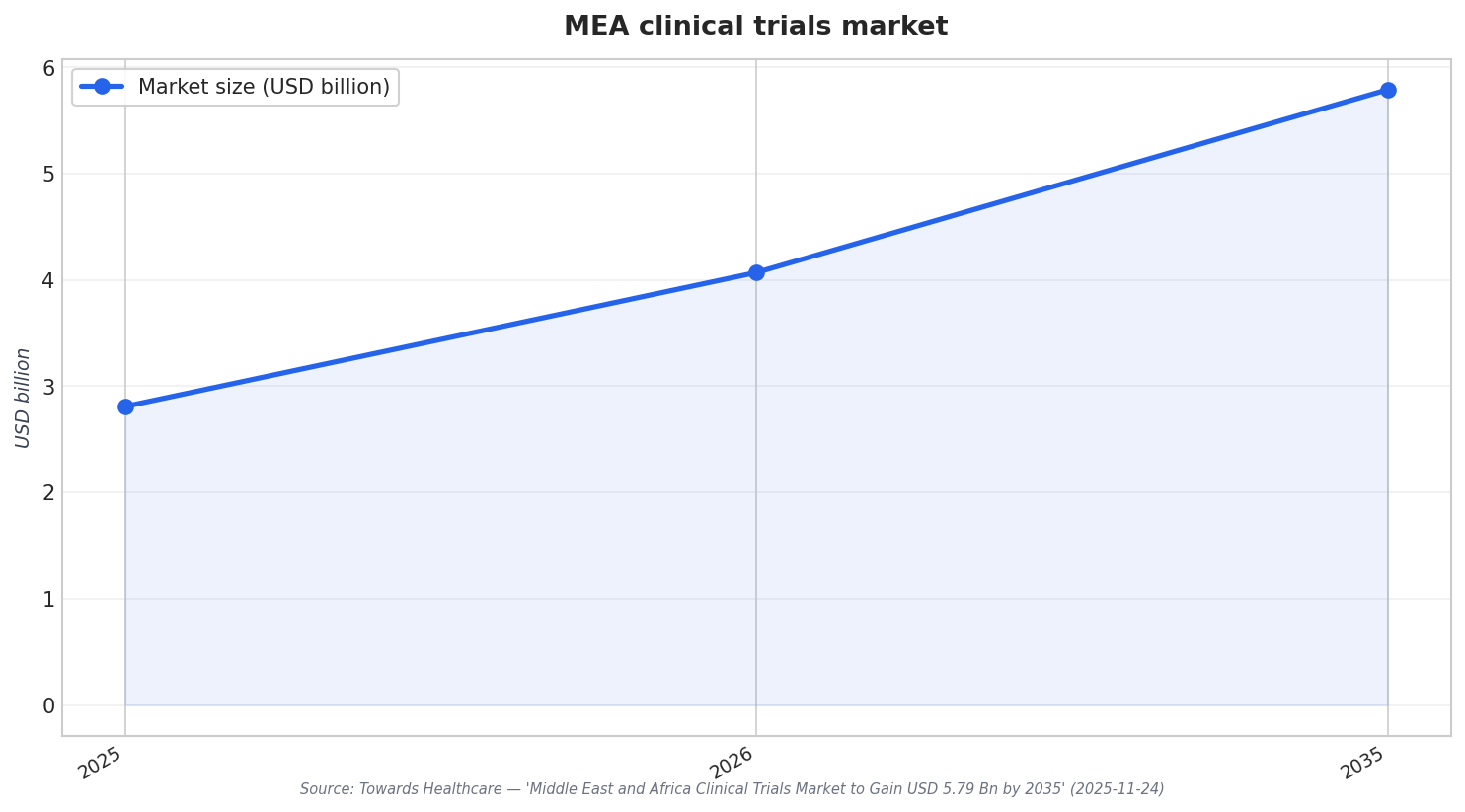

Saudi Arabia’s rise should also be read in regional context, not isolation. Another regional outlook puts the Middle East and Africa clinical trials market at US$ 2.81 billion in 2025, forecasting US$ 4.07 billion in 2026 and nearly US$ 5.79 billion by 2035, at a 6.80% CAGR. The same region is also adopting digital and decentralized clinical trials using telemedicine, wearables, and mobile applications; for comparison, Qatar committed approximately US$2.5 billion in 2025 under its “Digital Agenda 2030” to support AI and data initiatives that can facilitate DCT growth. With SFDA reforms, growing CRO services, and expanding CTMS adoption, the saudi clinical trials market is positioning itself as a more execution-ready destination for global and local sponsors.

What regulatory change is most associated with growth in Saudi Arabia’s clinical trials activity?

How large is Saudi Arabia’s pharmaceutical CRO market according to the sources?

What figures indicate rising trial volume and supporting infrastructure in Saudi Arabia?

What disease burden drivers are cited for clinical research demand tied to Saudi Arabia and the region?

What is shaping the Saudi clinical trials market besides regulation?