The saudi IVF market is growing as fertility care becomes more visible and more accepted. IVF helps when natural pregnancy is difficult. It fertilizes an egg with sperm outside the body in a lab. The embryo is then monitored and transferred to the uterus to support implantation and pregnancy. Sources also describe related steps that may be used, such as hormone therapy, genetic testing, egg harvesting, and embryo freezing.

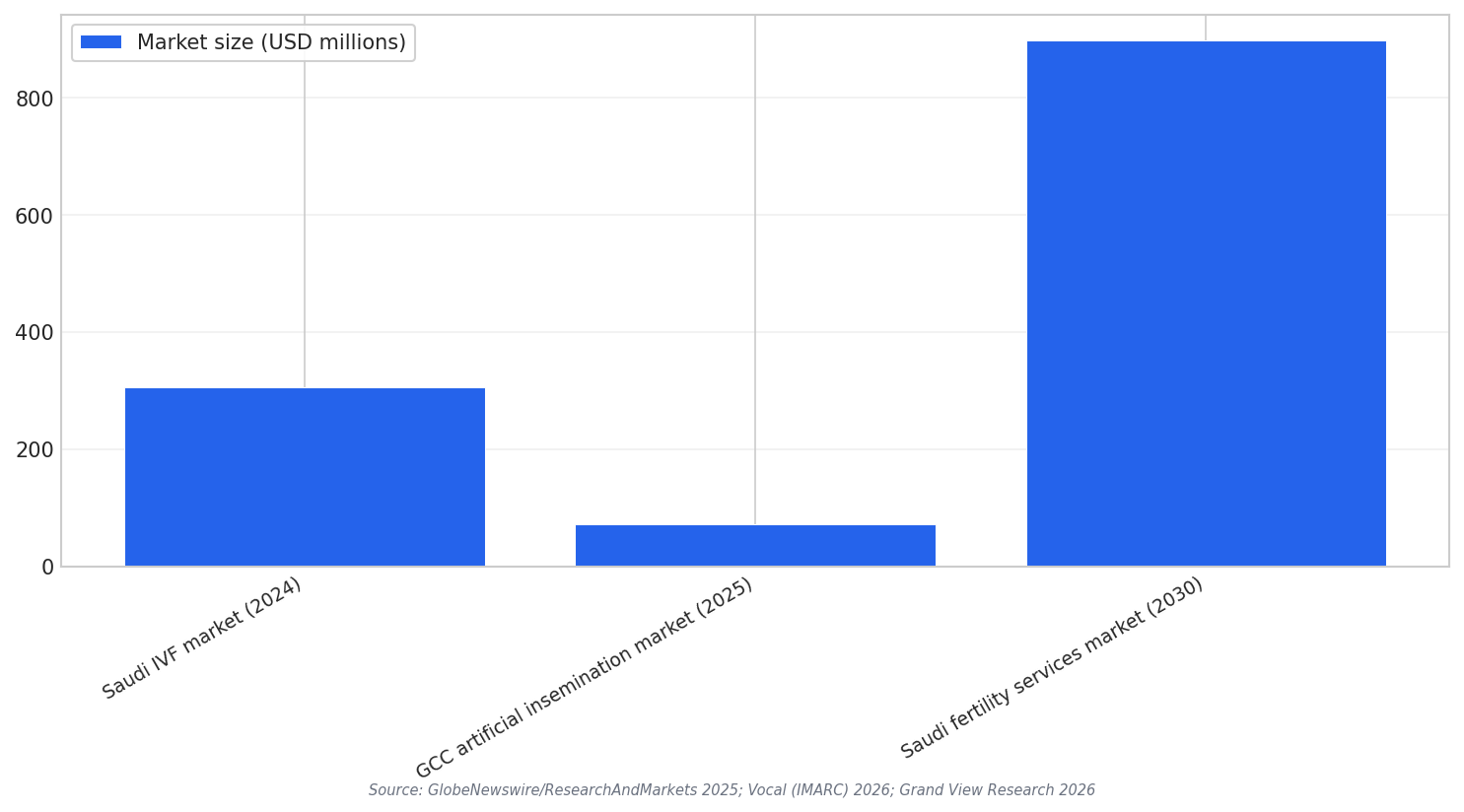

Market forecasts in the sources point to steady expansion. One report states the Saudi Arabia IVF market is expected to reach US$ 522.39 million by 2033, up from US$ 306.59 million in 2024, with a CAGR of 6.10% from 2025 to 2033. Another Saudi market dataset highlights how treatment choices can shift demand inside the market. It reports that the frozen nondonor segment was the largest segment with a revenue share of 48.27% in 2023.

The sources also include Saudi figures on the wider fertility space and on regional fertility-related services that can influence patient pathways before IVF. Grand View Research says the fertility services market in Saudi Arabia is expected to reach US$ 897.6 million by 2030. A separate GCC source says the GCC artificial insemination market was valued at USD 72.9 million in 2025 and is estimated to reach USD 138.4 million by 2034.

What Is Driving Demand in Saudi Arabia

Delayed parenthood is a repeated theme in the sources. They link it to more people focusing on education, careers, and financial stability before starting a family. The sources also connect delayed motherhood with age-related fertility decline, which can make IVF more necessary. Lifestyle changes and stress are also described as reasons for higher infertility rates, along with delayed marriage.

Medical progress is another driver. The sources mention improving success rates through reproductive technology advances such as genetic screening, freezing embryos, and intracytoplasmic sperm injection (ICSI). They also describe IVF being used for causes including male-factor infertility, blocked or damaged fallopian tubes, ovulation disorders, endometriosis, unexplained infertility, and age-related fertility decline.

Providers also benefit from broader system changes. The sources cite supportive government policies, subsidies, and supportive healthcare legislation. They also point to higher healthcare investments and improved healthcare infrastructure. One GCC-focused source adds that Saudi Arabia is investing over 224 billion USD in public health infrastructure development, and it links infrastructure upgrades and specialized clinics to better access. The sources also mention growing medical tourism and shifting cultural perceptions toward fertility treatments, which can increase demand and clinic competition through 2026 and beyond.

What is the expected growth path for the saudi IVF market in the sources?

Which IVF segment is highlighted as the largest in Saudi Arabia?

What are the main demand drivers mentioned for IVF in Saudi Arabia?

How does artificial insemination relate to the fertility landscape in the region?