Saudi Arabia’s move toward a more unified payer structure is unfolding alongside wider healthcare reforms under Vision 2030. The country accounts for 60% of Gulf Cooperation Council (GCC) healthcare expenditure, and healthcare remains a stated government priority. In 2024, the Saudi government allocated SAR 214 billion (about US$57.1 billion) to the healthcare sector, around 17% of the total budget. At the same time, Vision 2030 includes a planned US$13.8 billion investment in medical facilities by 2030. This context matters for understanding how Saudi national health insurance reforms are being designed to support long-term system transformation.

Institutionally, the Ministry of Health is described as the regulator for healthcare activities and services, having transitioned away from its previous role as provider. Day-to-day healthcare administration and primary care development programs sit with the Health Holding Company (HHC), which also includes expanded digital health and virtual care. The Center for National Health Insurance (CNHI) is positioned as a payer entity that will provide payment for health services delivered by HHC and its subsidiaries. Trade guidance describes CNHI as financed by the Ministry of Finance and tasked with strategically procuring services and engaging in contractual partnerships with health clusters to deliver free, high-quality care tailored to individual needs.

What Changes as CNHI Becomes the Main Budget Holder

Independent analysis of the healthcare and HTA landscape expects CNHI to become the main budget holder for healthcare services by 2027, overseeing funding for health clusters and other public institutions. That anticipated transfer of funding responsibility is described as part of a large-scale transformation tied to the broader shift to the HHC model. The same source emphasizes that integrating HTA with reforms to healthcare delivery and financing, including the evolving roles of HHC and CNHI, will be essential during the change period. In the current structure, Saudi citizens receive full coverage across primary, secondary, and tertiary care levels, including medications, while health insurance is mandatory for non-Saudis and is typically employer-provided for employees and dependents.

Market indicators show rapid motion in insurance financing and provider payment tools as the CNHI model ramps up toward the 2026 timeframe. One industry white paper values Saudi Arabia’s healthcare market at SAR 260 billion in 2025 and reports private health insurance premiums reached SAR 42.2 billion in 2024 after rising 9% year-on-year. The paper also argues that full activation of CNHI and the rollout of Diagnosis Related Groups (DRG) will redefine hospital funding by linking payments to quality, efficiency, and outcomes rather than volume. In parallel, insurers and providers are modernizing processes through real-time e-claims on the NPHIES platform, which is described as improving settlement speeds and reducing working-capital pressures.

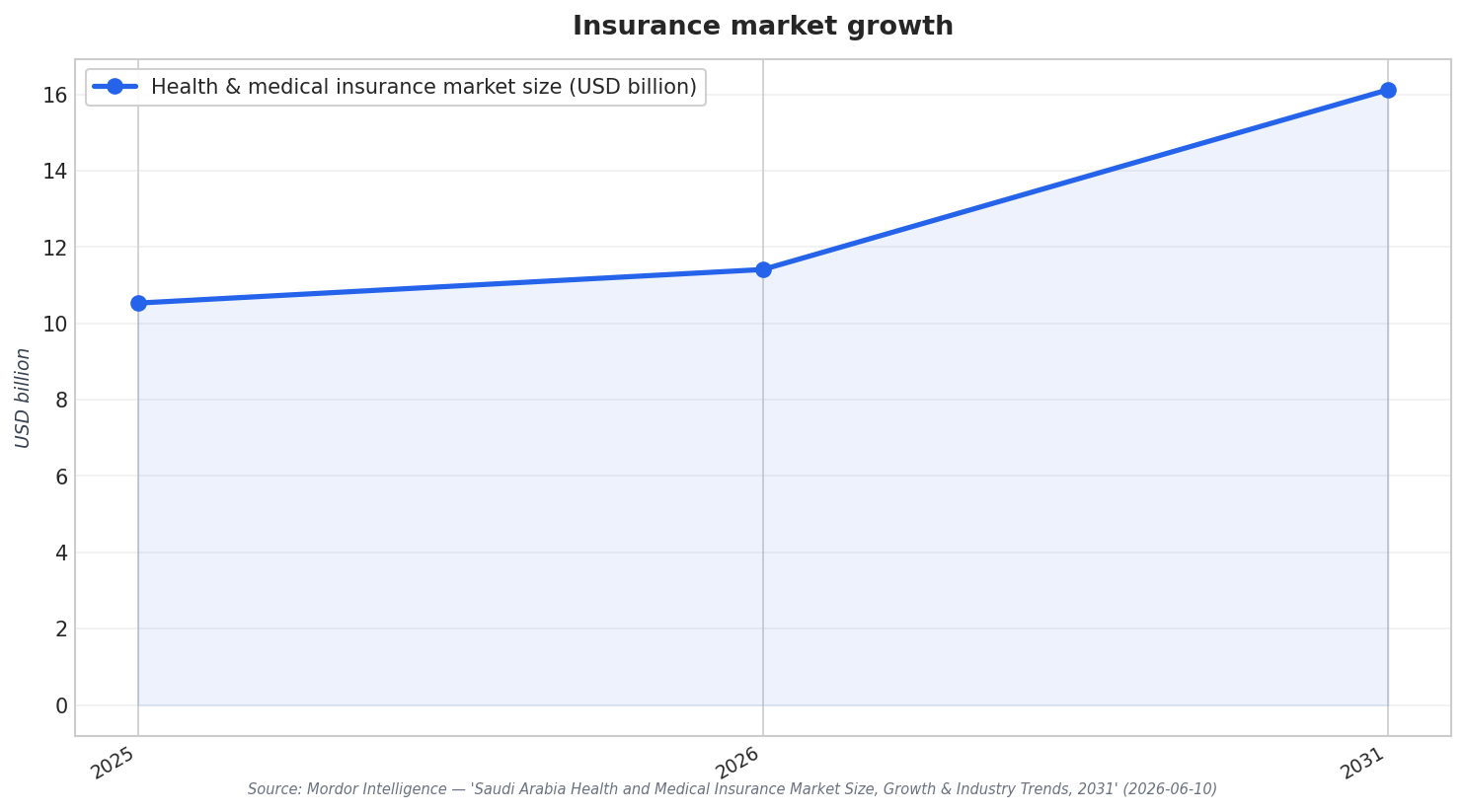

Forecasts for the health and medical insurance market also point to continued expansion as governance and digital adoption increase. One market report values premium volume at USD 10.53 billion in 2025, estimating growth from USD 11.41 billion in 2026 to USD 16.12 billion by 2031 at a 7.16% CAGR (2026–2031). It also notes the Sehhaty mobile health application has over 24 million users, around 68.5% of the population, highlighting strong mobile health adoption. Another outlook projects Saudi Arabia’s healthcare insurance market reaching US$19,709.7 million by 2033 and expects a 5.3% CAGR from 2026 to 2033. Together, these signals frame the operational and financial runway for CNHI-style purchasing and contracting to mature.

What is CNHI supposed to do in Saudi Arabia’s healthcare reforms?

When is CNHI expected to become the main budget holder for healthcare services?

How does coverage differ for Saudi citizens versus non-Saudis?

What do recent figures show about private health insurance premiums in the Kingdom?

What should readers know about the Saudi national health insurance direction and digital readiness?