Saudi Arabia’s obesity challenge is reshaping how weight management is discussed and delivered. A 2026 Saudi Healthcare Consulting guide describes a new boom in medical weight management, with more people seeking clinical care rather than only diet advice. In 2024, 42.6% of individuals aged 15 years and older in Saudi Arabia were classified as overweight, and 23.1% were classified as obese. For regional context, the same source cites a 2022 Middle East study that found 33.1% overweight and 21.2% obese. Together, these figures explain why treatment pathways are expanding across medications, surgery, and clinic-based wellness programs.

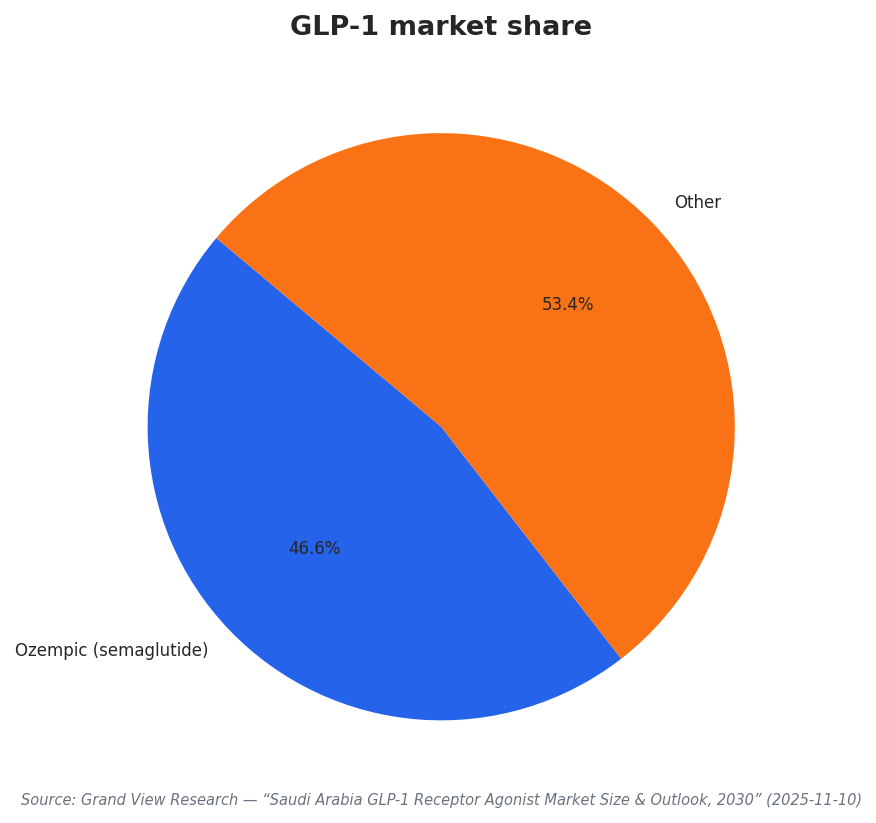

Pharmacotherapy is a central pillar of the emerging Saudi obesity treatment market, with GLP-1 receptor agonists frequently cited as a major driver of demand. In Saudi Arabia, Grand View Research estimates the GLP-1 receptor agonist market generated USD 181.3 million in 2024 and is expected to reach USD 415.6 million by 2030. Within that market, Ozempic (semaglutide) held a 46.61% revenue share in 2024. On outcomes, a 2024 study from King Abdulaziz University reported that patients using GLP-1 medications lost an average of 10.11 kg, while international research cited in the same guide notes the STEP-1 trial found an average 15% reduction in body weight over 68 weeks with weekly semaglutide injections in people without diabetes.

Access, Costs, and Care Models Will Shape the Next Phase

Even as GLP-1 adoption grows, systemic barriers can slow real-world uptake and continuity of care. A 2026 BMC Public Health analysis states that the introduction of novel anti-obesity medications, such as GLP-1 receptor agonists, has been slowed by high costs and limited insurance coverage. The same study also notes that primary care systems may lack infrastructure for comprehensive obesity management, and some providers remain inadequately trained in evidence-based obesity treatment approaches. These constraints matter because the clinical need is broad, and the obesity challenge is commonly accompanied by chronic conditions, raising the importance of structured pathways that can be scaled beyond specialist centers.

Bariatric surgery remains a major option, but availability is uneven. The BMC Public Health study reports that bariatric surgery rates have increased in recent years, yet access remains limited primarily to major urban centers. A Saudi Healthcare Consulting summary also highlights a meta-analysis of five cohort studies cited in an Eastern Province study, which found bariatric surgery was linked to lower risks of all-cause mortality, major adverse cardiovascular events, and heart failure compared with GLP-1 therapy, while noting that randomized trials are needed for clearer comparisons. Alongside hospital pathways, wellness and aesthetic clinics are also marketing weight-loss injections, and one Riyadh provider claims “13+ years of experience” and a “more than 90% success rate of all procedures,” while describing higher-dose semaglutide for weight management.

Market development is also being shaped by policy and channel expansion. Ken Research values the Saudi Arabia Obesity Treatment Devices and Therapeutics Market at approximately USD 52 million and notes that Riyadh, Jeddah, and Dammam dominate due to infrastructure and access. Ken Research also states that in 2023 the Saudi government implemented the National Strategy for Obesity Control, promoting evidence-based protocols and aiming to improve access. Beyond medications and surgery, Ken Research points to behavioral therapy, nutritional counseling, digital therapeutics, and telemedicine services as active growth themes, alongside a rising preference for non-invasive options such as gastric balloons and lifestyle modification programs.

What do recent figures say about overweight and obesity in Saudi Arabia?

How much weight loss has been reported with GLP-1 medications in a Saudi study?

How large is Saudi Arabia’s GLP-1 receptor agonist market, and what is a key product share?

What barriers are slowing anti-obesity medication access in Saudi Arabia?

What is the current value cited for the Saudi obesity treatment market in devices and therapeutics?